Every company in India shares one obligation that has nothing to do with how much it earns, how big it is, or whether it made a single rupee this year. It must get its books audited. Not the profitable ones. Every one.

That obligation is the statutory audit and it's the single most misunderstood compliance requirement among founders and small business owners. Many treat it as a year-end formality handed off to a Chartered Accountant and forgotten. In reality, it's the mechanism that decides whether you’re financial statements can be trusted by banks, investors, tax authorities, and the Registrar of Companies.

This guide breaks down exactly what a statutory audit is, who it applies to, how the process runs, what happens if you skip it, and how it differs from the tax audit and internal audit people constantly confuse it with.

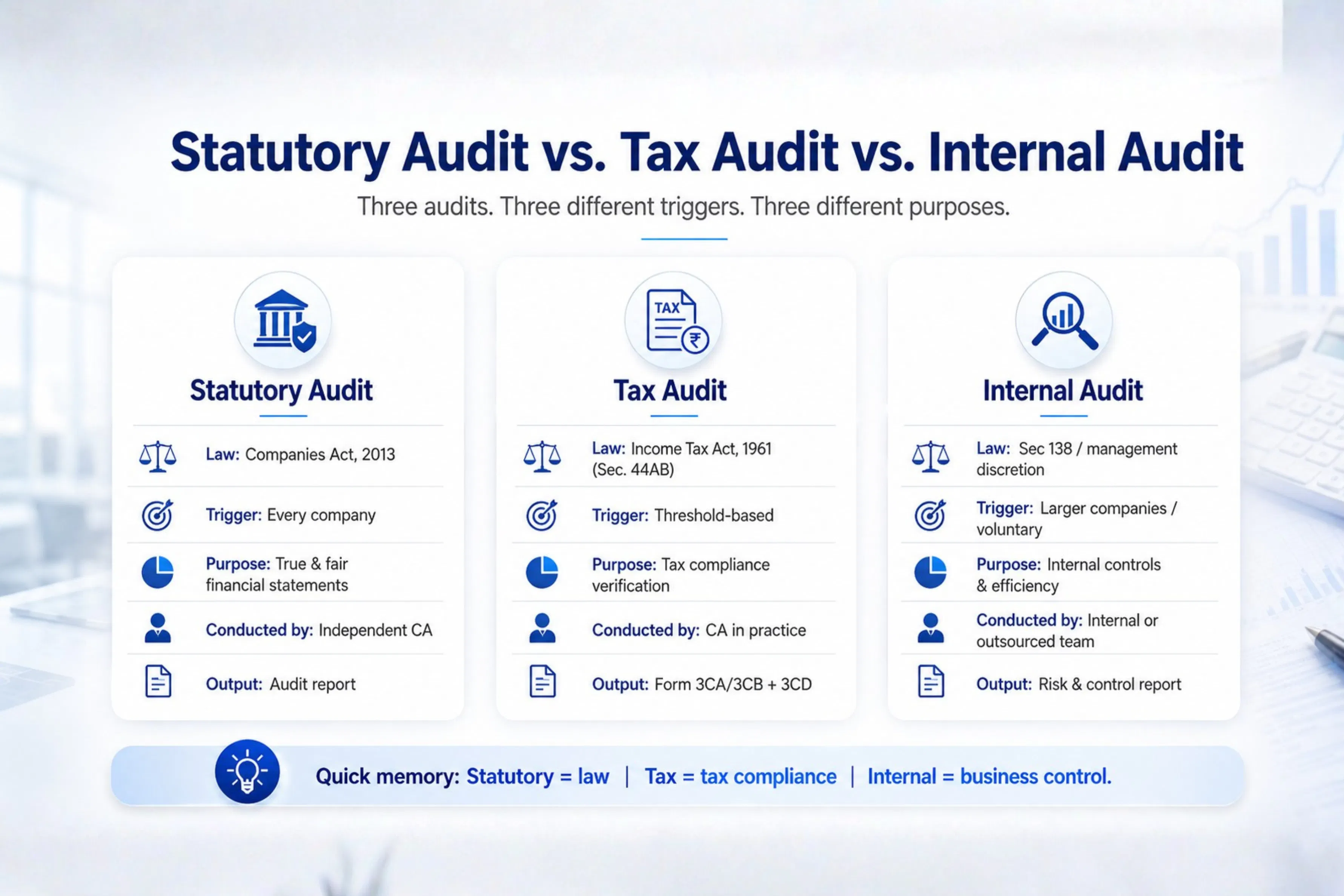

What is a Statutory Audit?

A statutory audit is a legally mandated independent examination of a company's financial statements by a qualified Chartered Accountant, carried out to confirm that those statements present a true and fair view of the company's financial position.

In plain terms, it answers one question for every outside party who reads your accounts: “Can we believe these numbers?”

The word that matters is statutory it means the audit is required by law, not chosen by management. It is governed primarily by the Companies Act, 2013, and conducted in line with the auditing standards issued by the Institute of Chartered Accountants of India (ICAI).

A statutory audit isn't an opinion on whether your business is doing well. It's an independent verdict on whether your financial statements can be trusted.

Who Needs a Statutory Audit in India?

This is where most confusion begins. Under Sections 139 and 143 of the Companies Act, 2013, every company registered in India must undergo a statutory audit regardless of turnover, profit, or size.

That means:

• Private Limited Companies :- audit mandatory from day one

• Public Limited Companies :- audit mandatory

• One Person Companies (OPCs) :- audit mandatory, even with a single member

• Section 8 (non-profit) companies :- audit mandatory

Crucially, a dormant company with zero activity, or a company running at a loss, is not exempt. If it is registered under the Companies Act, its financial statements must be audited every financial year. There is no turnover threshold to hide behind.

What about LLPs and proprietorships?

Limited Liability Partnerships (LLPs) are governed by the LLP Act, 2008, not the Companies Act. An LLP requires a statutory audit only if its annual turnover exceeds ₹40 lakh or its capital contribution exceeds ₹25 lakh. Below both limits, the audit is optional.

Sole proprietorships and ordinary partnership firms have no statutory audit requirement under the Companies Act at all. Instead, they may fall under the tax audit provisions of the Income Tax Act which is a completely different thing, and the source of endless mix-ups. We'll clear that up next.

The simplest way to hold it in your head: a statutory audit is about the law, a tax audit is about the taxman, and an internal audit is about you.

One more point that trips people up: if a company is already covered by a statutory audit under the Companies Act, it does not audit its accounts twice. It simply files the additional tax audit report in the prescribed format where Section 44AB applies.

How the Auditor is appointed

A statutory auditor isn't someone you casually engage. The Companies Act sets a strict procedure under Section 139:

1. First auditor: appointed by the Board of Directors within 30 days of incorporation.

2. Subsequent auditor: appointed by shareholders at the Annual General Meeting (AGM), usually for a term of five years.

3. Filing: the company files Form ADT-1 with the Registrar of Companies to record the appointment.

4. Eligibility: only a practising Chartered Accountant, or a firm where the majority of partners are practising CAs, can be appointed. The auditor must be independent no financial interest in the company.

Larger and listed companies also face auditor rotation rules under Section 139 to prevent long, cosy relationships between a company and its auditor from eroding independence.

The Statutory Audit Process - Step by Step

A well-run statutory audit follows a clear, repeatable sequence:

Step 1: Appointment and Engagement

The auditor is formally appointed and issues an engagement letter defining the scope, responsibilities, and reporting framework for the year.

Step 2: Understanding the Business and Controls

Before touching a single ledger, the auditor studies how the business operates, how transactions flow, and where the internal controls are strong or weak. This shapes where they look hardest.

Step 3: Risk Assessment and Audit Planning

The auditor identifies areas most prone to material misstatement revenue recognition, inventory valuation, related-party transactions and designs the audit procedures around those risks.

Step 4: Verification and Evidence Gathering

This is the core. The auditor examines vouchers, invoices, bank statements, contracts, and confirmations; tests balances; and gathers evidence to support every material figure. Under Section 143, the auditor has an unrestricted right to access the company's books, records, and explanations from officers.

Step 5: Compliance and Standards Check

Financial statements are tested against the applicable Indian Accounting Standards (Ind AS) under Section 129, and the audit itself is conducted per the auditing standards notified by ICAI and overseen by the NFRA.

Step 6: Reporting

The auditor issues the statutory audit report to the shareholders, stating whether the financial statements give a true and fair view, whether proper books have been kept, and flagging any qualifications, reservations, or adverse observations. If fraud is suspected above the prescribed limit, the auditor is legally bound to report it.

Step 7: Filing

Post-AGM, the company files Form AOC-4 (financial statements) within 30 days and Form MGT-7 (annual return) within 60 days with the Registrar of Companies.

Why a Statutory Audit Actually Matters

Strip away the compliance language and a statutory audit does something genuinely valuable it makes your numbers believable to people who have no reason to take your word for it. Here's why that pays off:

1. It Makes Your Financials Credible

An audited statement carries the independent sign-off of a Chartered Accountant. Banks, investors, and partners treat audited numbers as trustworthy and unaudited numbers as claims. That credibility is the entire point.

2. It Unlocks Funding and Credit

No bank sanctions a working capital loan and no serious investor writes a cheque on unaudited books. A clean statutory audit report is effectively the entry ticket to external capital.

3. It Detects Errors and Fraud Early

An independent set of eyes catches misstatements, control gaps, and irregularities that internal teams miss or overlook. Under the Companies Act, auditors carry a specific duty to report suspected fraud.

4. It Keeps You on the Right Side of the Law

Filing audited financials via AOC-4 and MGT-7 is mandatory. A missed or defective audit cascades into ROC penalties, director disqualification risk, and compliance flags that follow the company for years.

5. It Strengthens Governance and Decision-Making

Audited data is reliable data. When your balance sheet is verified, every decision built on it pricing, expansion, hiring, and investment rests on solid ground instead of guesswork.

6. It Smooths Due Diligence

Mergers, acquisitions, fundraising, and valuations all begin with someone examining your financials. A history of clean statutory audits turns a painful due-diligence process into a formality.

Unaudited numbers are a claim. Audited numbers are a fact. The gap between the two is where trust and money lives.

What Happens if You Skip It? (Penalties for Non-Compliance)

This is not a requirement to treat casually. Non-compliance under Section 147 of the Companies Act carries real consequences:

• The company can be fined between ₹25,000 and ₹5,00,000.

• Officers in default can face fines between ₹10,000 and ₹1,00,000.

• The auditor, for contravention, can be fined between ₹25,000 and ₹5, 00,000 and in cases of wilful intent to deceive, imprisonment of up to one year may apply.

Separately, failing to complete a required tax audit under Section 44AB of the Income Tax Act attracts a penalty under Section 271B of 0.5% of turnover or gross receipts, subject to a maximum of ₹1.5 lakh (being reclassified as a fee under recent Budget proposals to reduce litigation).

The math is simple: timely compliance is almost always cheaper than the penalty for skipping it before you even count the reputational cost.

Audits go smoothly for prepared companies and painfully for scrambling ones. Keep these seven ready and you'll turn a stressful season into a routine one:

1. Clean, reconciled books: - ledgers matched to bank statements, with no unexplained entries.

2. Complete documentation: - invoices, vouchers, contracts, and bills organised and retrievable.

3. Auditor appointed on time: - with Form ADT-1 filed and the appointment properly recorded.

4. Statutory registers updated: - members, directors, charges, and related-party disclosures current.

5. Tax and GST filings reconciled: - returns matching the books, input tax credit trails intact.

6. Prior-year observations closed: - last audit's recommendations actually acted on, not filed away.

Filing calendar mapped: - AGM, AOC-4, and MGT-7 due dates locked in before they arrive

How NextGen Helps Businesses with Statutory Audits

At NextGen Business Support Services Pvt. Ltd., we treat the statutory audit not as a box to tick, but as an opportunity to strengthen your financial credibility and close compliance gaps before they become problems.

Our audit and compliance support is designed to keep your company fully compliant under the Companies Act while making the whole process painless for your team.

Our Statutory Audit Support Includes:

End-to-End Statutory Audit Execution

Our Chartered Accountant-led team conducts the full statutory audit from planning and risk assessment to verification and final reporting in line with ICAI auditing standards and the Companies Act, 2013.

Auditor Appointment & ROC Compliance

We manage the appointment formalities including Form ADT-1, and ensure your AOC-4 and MGT-7 filings are prepared and submitted within statutory timelines so you never miss a due date or invite a penalty.

Financial Statement Preparation & Ind AS Compliance

We help prepare and finalise financial statements that comply with the applicable accounting standards, so what goes into the audit is already accurate and defensible.

Internal Control & Compliance Review

Beyond the audit itself, we assess your internal controls, documentation practices, and approval mechanisms to identify weaknesses and reduce audit risk in future years.

Tax Audit Support under Section 44AB

For businesses crossing the Income Tax Act thresholds, we handle the tax audit and Form 3CA/3CB and 3CD reporting alongside the statutory audit one coordinated engagement instead of two disconnected ones.

Audit-Readiness for Startups & Growing Companies

For newly incorporated companies, OPCs, and startups navigating their first audit, we set up clean processes from the outset so compliance scales smoothly as you grow.

Detailed, Action-Oriented Reporting

Our reports don't stop at the audit opinion. They flag control gaps, compliance risks, and practical improvement points that management can actually use.

Why Businesses Choose NextGen

• Experienced Chartered Accountant-led audit team

• Full Companies Act, Ind AS, and Section 44AB compliance under one roof

• PAN-India execution capability

• Coordinated statutory + tax audit no duplication, no gaps

• On-time ROC filings (ADT-1, AOC-4, MGT-7) with zero missed deadlines

• Support for management, investors, banks, and internal stakeholders

A statutory audit should do more than satisfy the law it should give you financial statements you can stand behind with total confidence. At NextGen, that's exactly what we deliver: clean, compliant, credible books, on time, every year.

The Bottom Line

A statutory audit isn't the price you pay for running a company it's the proof that your company can be trusted. It converts your own accounts into an independently verified fact that banks lend against, investors bet on, and regulators accept.

So the real question isn't whether your business needs a statutory audit. If you're a company in India, the law already answered that. The question is: when someone finally examines your numbers, will they find a company that's ready or one that's scrambling?

Need your statutory audit handled cleanly and on time?

Book a free consultation with NextGen and let's make compliance the easiest part of your year.

Book a Consultation Today!

Free consultation • Fast response

Let’s discuss your growth plan

Share your requirements and we’ll suggest the best next steps for your store, ads, and performance.

- Store & catalog review

- Ads & ROAS audit

- Setup & onboarding

- Actionable roadmap

Prefer email? care@nbsspl.com